Address of the President

Address of the President

175th Anniversary of Russian Railways

175th Anniversary of Russian Railways

Analysis

Analysis

Save Key Indicators to XLS

Save Key Indicators to XLS

Transport Development Strategy

Transport Development Strategy

Investment Activity

Investment Activity

Download Chapter Financial and Economic Performance

Download Chapter Financial and Economic Performance

Rating

Rating

Loan Portfolio

Loan Portfolio

Management System

Management System

Governing Structure Of JSC Russian Railways

Governing Structure Of JSC Russian Railways

Personnel management

Personnel management

Housing policy

Housing policy

Service functions

-

Download center

-

Add to My Report

-

My Report (0)

-

Print this Page

-

Download in PDF

-

Share

-

Feedback

-

Interactive analysis

-

Browsing history

-

Offline version

-

Company in soc.networks

-

Compared to 2011

-

Popular pages

-

Company on the map

-

Compact view

| Enter e-mail recipient * | Your e-mail * | Comment : | |

| * required fields | |||

State Tariff Policy: New Rules with Regard to JSC “RZD”

Major changes in the freight transportation tariff regulation will take place in 2013 with regard to the unification of the tariff policy of Common Economic Space member states. In 2013, JSC “RZD” was vested with a right to use a flexible tariff regulation mechanism.

On 1 November 2012 a decree of the Russian FST came into force on the unification of tariffs for the empty running of all-purpose open cars and platforms and special-purpose platforms for timber transportation less than 19.6 meter long irrespective of earlier transported freight. The stopping of the previous practice (when empty car transportation cost was dependent on the class and type of the transported cargo) has enabled the improvement of track process conditions: the number of empty open cars and occupied platforms after unloading highincome freight has nearly halved, which is evidence of a decrease in empty backhaul.

Tariff unification of CES member states

The Russian Federation, Republic of Belarus and Republic of Kazakhstan continued their work as a part of the Agreement on the regulation of access to rail transport services, including basic principles of the tariff policy.

The Agreement was signed in December 2010; it provides for the unification of the countries’ tariffs by service types (exports, imports and domestic tariffs for freight railway transportation services). A country’s tariff applies to internal transportation, and unified tariffs of each country apply to transportation between Agreement member states or transit through their territory to third countries. The Regulation came into force on 1 January 2013.

Tariff unification was completed in 2012. The Russian Federation has implemented the international arrangements and, since January 2013, freight transportation has been conducted in accordance with the common tariff calculation methods (section 2 of Pricelist No.

In December 2012, the Eurasian Economic Committee approved the Rules of access to infrastructure services and the Rules of provision of infrastructure services as a part of the Common Economic Space. These Rules must now be coordinated with the public authorities of Agreement member states.

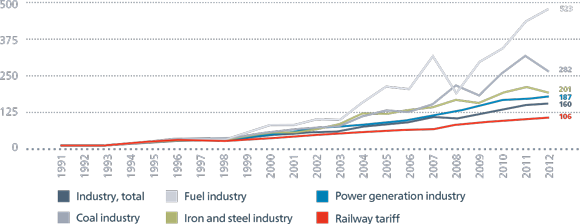

DYNAMICS OF PRICE INDICES AND TARIFFS FROM 1991 TO 2012, GROWTH VERSUS DECEMBER 1990, TIMES

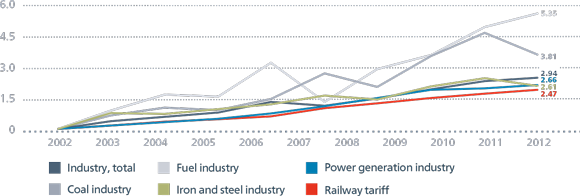

TRENDS OF INDUSTRIAL MANUFACTURING PRICE INDICES AND TARIFFS SINCE 2003 (GROWTH VERSUS DECEMBER 2002, TIMES)

Long-term effects of low tariffs: railways effectively subsidizing other industries

Restrictive measures of tariff regulation still apply to federal rail transport. This has effectively led to a subsidy of other industries at the expense of railways and a shortage of investment resources in the rail transport industry. By way of comparison, from 1991 to 2012, the railway tariffs index was 106. Over the same period, industry prices increased:

- overall, by 162 times;

- in the fuel industry, by 561 times;

- in the coal industry, by 320 times;

- in the iron and steel industry, by 215 times;

- in the power generation industry, by 176 times.

Shortage of investment resources required for the replacement and development of railway fixed assets has resulted in significant overload in many areas, resulting in difficulties for businesses.

In December 2012, Russian FST also issued decrees to approve the Guidelines for the determination of price limits (maximum and minimum) with regard to rail transport service tariffs, procedures and terms of use (determination, revision) of the rail transport service tariff level for freight transportation within price limits (maximum and minimum) and price limits for average network conditions.

In 2013, JSC “RZD”, may use a flexible tariff regulation mechanism — from 0.872 to 1.134 (decree No. 423-t/3 dated 21 December 2012).

Pricelist No.

Changes in freight and passenger transportation tariffs in 2012

During 2012, the following tariffs were increased:

- freight railway transportation (annual average increase of 6%);

- long-distance passenger transportation in the regulated segment (couchette and general cars) +10%;

- in the deregulated segment (saloon and sleeping cars) +5%.

For reference: in 2012, the consumer price index increased 5.1% (annual average).

Currently, the car component of third party-owned rolling stock use is not subject to regulation and is determined by them at their discretion. Current market prices resulted in an excess of the cost of freight transportation by third-party owned cars over the tariffs set out in Pricelist No.

Transport component cost of finished products is decreasing

Price inflation in most industries is rising more quickly than the railway price tariffs, which results in a decrease in the cost of the transport in the overall price of products transported by rail transport.

At the same time, the share of logistic costs in Russia’s GDP remains excessively high: about